How do consultants determine their fees?

I’ve often received judgmental remarks from employees and managers about the “outrageous” rates charged by consultants. Although in many cases it seems a waste of time to try and explain why you can’t simply compare an employee’s wage rate with the fee of an independent contractor, I decided to do it again today.

Be warned, this is an explicit and long one to read!

Things to consider as an independent contractor in the province of Quebec, Canada

Salary

Self-employed (individual) or incorporated contractor (company), the gross annual salary protects the current standard of living and must not decrease. Contract workers must generate enough income to cover their gross salary.

Benefits

Certain expenses normally borne by an employer are borne by the independent contractor. To maintain the same level of contribution to a pension plan, and to maintain insurance to cover a portion of medical expenses, health costs and the risk of disability, the portions paid by the employee and his employer will have to be fully covered in addition to the salary in its calculation.

Group insurance costs approximately 4% of an employer’s gross payroll, covered 50% by the employee. If a self-employed person cannot be covered by the spouse’s employer’s plan, he or she will have to turn to personal life, dental and medical insurance programs that are complementary to RAMQ. These programs easily cost $200 a month.

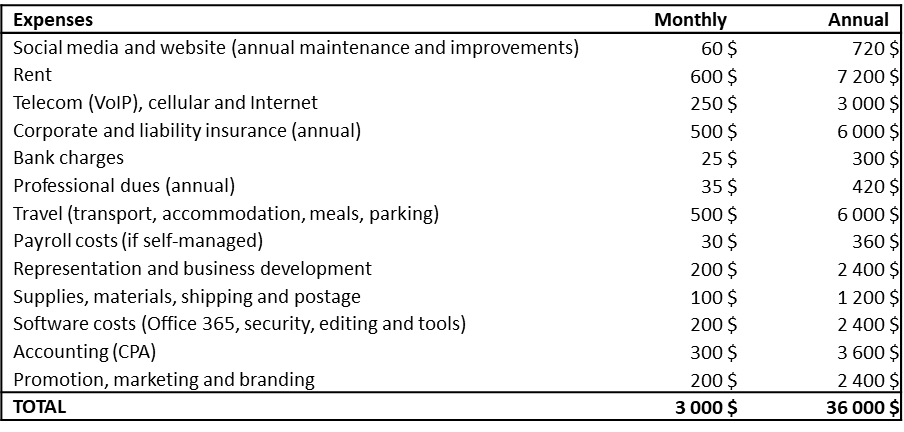

Costs related to self-employment

Independent contractors have to cover several expenses that are normally covered by employers. In 2023, in Quebec, an independent contractor must budget between $20,000 and $50,000 in operating expenses per year (before taxes). Here’s a representative example of annual expenses for an incorporated contractor:

This example offers an interesting perspective, but it should be noted that the figures and specific categories do not apply to all independent contractors. Individual situations vary considerably, and it is essential to take account of each individual’s reality.

Billable days

A permanent salaried employee is guaranteed to receive 26 payments covering 260 days at his or her wage rate, without fail from his or her employer. Like an hourly employee, an independent contractor is only paid for the days worked for a customer (billable days), and this is where the comparison with permanent salaried employees gets tricky. You need to calculate your rate solely based on days that will generate income.

An independent contractor receives no income for public holidays, vacations and absences due to illness or professional development. If he reserves 40 non-working days per year, he must reduce his calculation base from 260 days to 220 days.

What’s more, the contractor will inevitably have to spend time managing and developing his business. Unless this takes up personal time, additional non-billable time will have to be set aside. It’s wise to allow 6 to 12 days a year for this purpose, but this may not be enough if you have to do a lot of networking and self-promoting for your services. This further reduces the calculation base to around 210 billable days.

Of course, to avoid non-billable days, the contractor can delegate to other professionals, but this will add to his annual costs.

Unforeseen events and downtime

Another important consideration is that independent contractors rarely manage to bill 100% of their billable days each year. No one is immune to the unpredictability of the economy, or to early contract cancellation. In fact, regularly billing 90% or more only happens to contractors who accept full-time, long-term, renewable contracts. Planning your rate on the assumption of 100% billability is unrealistic.

90% billability is normally considered excellent, good from 75% and average from 60%. Occasionally, we experience periods of backlash, which can result in a drop to 60% or less (you know COVID-19?). Rule of thumb: a 10% drop is equivalent to around 20 days without billing (1 month).

As a general rule, it is advisable to plan with a billing rate of no more than 80%. Billing at 75% reduces the number of billable days from 210 to less than 150.

Profit margin and taxes

Basically, to establish the break-even point, we don’t consider a profit margin when setting an independent contractor’s rate. This margin is added to the prime rate to determine the “selling” rate, the one he will propose to his customers.

Independent contractors must register for taxes and collect GST and QST on every invoice, whether incorporated or not. He must remit the taxes collected to the government, and may keep the equivalent of the taxes paid on his operating expenses (the famous CTI and RTI) as compensation. In other words, taxes offer no personal financial advantage.

As far as income taxes are concerned, if 100% of annual operating expenses are deductible from income, the total tax payable by the contractor will essentially be on the gross salary through his personal tax return. This is also true for an incorporated contractor who pays himself a dividend rather than a salary.

A contract worker who decides to incorporate and pay himself a salary will have to add to his calculations the employer’s contributions (9% of his salary in EI, QPP, RQAP, FSS) as well as additional payroll, accounting and legal fees that can represent more than $5,000 a year. In this case, he will have to add around $15 to his basic hourly rate.

Added value

A contractor’s rate must also account for his or her added value. The rarity of his expertise, his level of experience, his level of productivity, his professional certifications, and the environment in which he offers his services must be taken into account over and above the base rate. An ability to accomplish high-quality work in less time than others usually works against you on an hourly billing basis.

Work now, get paid later!

Freelance contractors are rarely paid on the same scale as employees. It is very common for a contractor to carry out work during the month, issue an invoice at the end of the month and be paid 30 to 60 days later. He must therefore plan a cash flow where cash inflows are shifted 2 to 3 months into the future.

When he starts out, he also needs to make sure he has enough funds to cover his salary and all his expenses for the first 2-3 months of work. In the fourth month, he will also have to reimburse the government for all taxes invoiced during this period, even if customers have not yet paid their bills. This is the effect of accrual accounting, which records accounting transactions as they occur (e.g., invoice issue date), without taking into consideration when the sums are received. Accrual accounting is the generally accepted accounting method in Canada.

Third-party premium

Today, it’s becoming increasingly difficult to obtain contracts directly from customers. Many obtain their mandates through one or more firms, notably because of framework agreements; firms pre-qualified at rates prescribed by type of professional service over several years.

These agreements give a limited number of firms a monopoly on mandate opportunities with major customers. To meet high-volume demand within prescribed deadlines, they use independent contractors. To compensate, they add a premiums to their subcontractors’ rates. This premium puts pressure on the rates of independent contractors, and is not always proportional to the actual contribution of the third party in the relationship between the independent contractor and the paying customer. But it is rarely possible to bypass this “systematic mechanism”.

The premium also contributes to the paying customer’s perception that “the contractor is very expensive” when, in fact, he receives only a portion of the rate billed by the third-party firm to paying customers.

The formula for a daily or hourly rate

The prime rate is your daily break-even point based on your assumptions. We derive the hourly rate according to the number of hours worked each day for the customer under each agreement.

Base rate = (Salary + Benefits + Expenses) / billable days after contingencies and downtime

The selling price takes into account your profit objectives and your added value. The latter is highly subjective and must be assessed according to the value of the mandate in the eyes of each customer.

Selling rate= Base rate + profit margin + value added by the contractor

The rate visible to the customer may be your selling rate, but mandates obtained through third parties carry a surcharge the size of which you will rarely know.

Customer rate = Selling rate + third-party surcharge

Quick methods for determining rates

There are several ways to quickly estimate the rate an independent contractor should charge his customers. Here are two of them.

The % of annual salary method

This method multiplies the contractor’s target gross annual salary by a factor of 0.7% up to a factor of 1.3%. The 0.7% factor corresponds to the minimum daily rate that the contractor must charge if he plans to bill 100% of his billable days and expects to spend no more than his annual budget. The 1.3% factor corresponds to a rate for billable occupancy in the 50% to 60% range. The 1% factor corresponds to the suggested rate for 70% occupancy,

Daily wage rate ratio method

This method begins by determining the gross salary rate. The target annual salary is divided by 260 days to obtain the daily salary rate. This rate is then multiplied by 2 to 5 to obtain the daily rate. A multiplier of 2 corresponds to a minimum viable rate with 100% billable occupancy. A multiplier of 2.2 to 3.0 is generally recommended for billable occupancy in the 60% to 80% range.

Comparison of methods

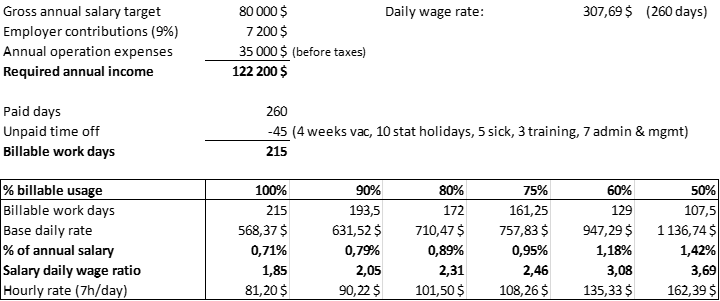

Let’s make the following assumptions:

- the contractor is incorporated and the company pays him a salary as an employee, so the company is obliged to collect deductions at source from the gross salary and pay employer contributions (± 9%), in addition, like any other employer

- benefits from 38 days of paid vacation, i.e. 4 weeks of vacation (20 working days), 10 statutory holidays, 5 sick days and 3 training days

- expects to be absent at least the equivalent of 7 days per year for management, administration and business development purposes

- estimates annual costs of approximately $35,000, plus taxes

- assesses different daily rates based on billable occupancy ranging from 100% to 50%.

- no expected profit margin.

For a gross annual salary of $80,000, we get:

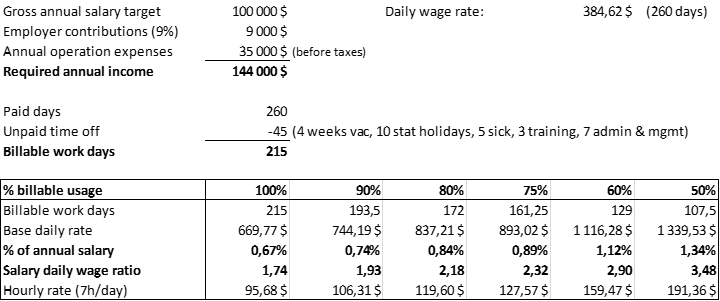

For a gross annual salary of $100,000, we get:

Life beyond the daily or hourly rate

Although it’s the most widespread in Quebec, it’s important to note that daily or hourly rates aren’t the only possible approach. Some contractors prefer to offer their services on other bases. Here are a few examples:

- Time and materials: the contractor invoices the costs and expenses associated with his intervention in addition to his fees.

- “Retainer: In this mode, the customer pays a fixed amount on a regular basis (e.g. monthly) to reserve the consultant’s services on an ongoing basis. This can be advantageous for consultants offering ongoing support or long-term advice.

- Fixed price: a pre-determined amount for a specific, clearly defined intervention, payable in instalments.

- Subscription: Contractors who provide ongoing services, such as technical support or maintenance, may charge their customers a periodic subscription fee for access to their services.

- Time bank: a fixed price for a certain number of hours available up to an expiry date. The time bank is often payable in advance to avoid abuse and negligence.

- Results-based: a pre-established proportion of the benefits arising from the contractor’s intervention. This mode is very difficult to manage because of the subjective nature of the “value of the benefit” and the difficulty of linking all this value to the contractor’s intervention.

The choice of billing method will depend on the nature of the work, the relationship with the client, the consultant’s personal preference and the way clients are willing to pay for services. Some consultants may also use a combination of these billing methods, depending on their different contracts and projects.

Conclusion

The world of independent contractors is complex, and their fees are justified by the realities of their business, the value of their input and the uncertainty they have to contend with. Before you judge, try to understand the challenges of freelance work.

As an example, here’s the simplified case of John.

John is a business analyst and a full-time employee. His employer pays him a salary of $80,000, 40 days off (holidays, vacation, illness, personal time, training, etc.) and contributes up to 5% of salary to his pension plan.

John is thinking of becoming an independent contractor. He wants a rate that will preserve the equivalent of his current conditions.

Self-employed individual: John will not create an incorporated company, but he will still have to register for federal and provincial taxes (GST/HST and QST). All of his income in a calendar year will therefore be taxable as an individual, and most of his work-related expenses will be deductible, but he won’t have to pay payroll costs, annual corporate fees or employer contributions like companies. He will, however, have to plan to pay his income tax, employment insurance, QPP, RQAP and RAMQ contributions after each calendar year, and start paying personal income tax instalments as of his second year of activity.

Salary: Jean will need to generate enough income to maintain a gross salary of $80,000.

Lost benefits: As a self-employed worker, John will have to assume the costs previously covered by his employer in pension contributions (5%) and group insurance costs (2%). This adds $5,600 to his required annual income.

Costs and expenses: John will have to cover his own costs for rent, communication, banking, equipment, supplies, software, travel, professional dues, accounting, marketing, etc. These costs average around $35,000 a year, if not more. These costs average around $35,000 a year, if not more. John is frugal and estimates his expenses at $20,000 a year.

Billable days: A contract worker only generates income when working for a customer. John must therefore subtract the 40 non-working days currently paid by his employer and add 5 days for business development and administration. John concludes that he has, at best, 215 billable days per year (260 – 45).

Unforeseen events and downtime: It’s unrealistic to expect John to be able to consistently bill 100% of his billable days. No one is immune to the vagaries of the economy or to early contract cancellation. Occupancy of 90% is normally considered excellent, good from 75%, average from 60% and bad if lower. John thinks he’ll manage to bill at least 161 days a year (75%).

John estimates that he’ll need an annual income of $105,600 billed over 161 7-hour days, or an hourly rate of at least $93.70. That’s more than double his employee wage rate, even with low expenses and no profit margin!

He finally realizes that contract rates reflect the need to cover many costs and uncertainties. The firms that control access to mandates offer him an hourly rate of $85 at most, and he won’t be paid for his work until 30 days after the end of each month worked! He should therefore expect to be without pay for the first 2 to 3 months of his transition, if he succeeds in drawing up a contract before leaving his job, or in his first month as a contract worker, which seems rather risky to him.

He also discovers that it’s very difficult to bypass these firms to get mandates, and that they all add a surcharge to his rate that leaves customers with the impression that he earns over $100 an hour.

Disillusioned, John finally decides to remain a full-time employee.

=> Can you figure what rate you would have to charge to maintain your current conditions of employment once you become an independent contractor?

© Eric Magnan, Pragmatik Advisory Services Inc, 2023

About the author:

Eric Magnan is a career consultant who founded Pragmatik Advisory Services in 2005. Since the late ’80s, he has assisted some 30 private and public companies through more than 70 missions aimed at adopting new technological solutions or new ways of working based on digital technology advances. He holds several professional certifications, which he puts down to good use for his customers through mission-driven commitments tailored to their context, constraints and needs.